US to cut minimum tariff on China shipments from 120% to 54%, China lifts ban on Boeing deliveries - Newsquawk US Market Open

- White House Executive Order said US will cut the minimum tariff on China shipments from 120% to 54%, and a minimum flat fee of USD 100 is to remain.

- European bourses are modestly firmer while US futures dip into the red. Focus this morning has been on Bloomberg reporting, which suggests China is to lift its ban on Boeing deliveries after the US-China tariff pause.

- DXY takes a breather to the benefit of other G10s; Antipodeans lead.

- EGBs and Gilts hit marginal new WTD lows, USTs await CPI & Trump.

- A subdued Dollar provides some modest strength for XAU/base metals.

- Looking ahead, US CPI, Speakers including BoE’s Bailey & ECB’s Rehn.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

TARIFFS/TRADE

- White House Executive Order said US will cut the minimum tariff on China shipments from 120% to 54%, and a minimum flat fee of USD 100 is to remain.

- USTR Greer said the outcome of US-China tariffs talks was seen as pragmatic, while he added China has agreed to remove countermeasures and noted if things don't work out, China tariffs can go back up.

- Chinese President Xi said there are no winners in tariff wars and trade wars, while he added that only when various countries work together can they maintain world peace, stability and promote global development. Xi said bullying and tyranny will only isolate oneself, as well as noted that China supports Latin America and the Caribbean in expanding their influence in the multilateral arena with China willing to deepen cooperation with Latin America in infrastructure, agriculture, food, energy and minerals.

- China's Foreign Ministry, on US fentanyl tariffs, says China has repeatedly said it is a US issue. US is ignoring China's good will. Responsibility lies with the US.

- US Treasury Secretary Bessent says talks with China in Geneva resulted in a mechanism to avoid escalation; can proceed from here and have a very good framework. When asked if he feels good about the progress of other deals, he responds "yes"; references Japan, South Korea, Indonesia, Taiwan. Thinks the US-Europe deal may be a bit slower, cites regional divides among the EU.

- Canadian PM Carney and UK PM Starmer agreed to strengthen trade, commercial and defence ties in a phone call, according to a statement from Canada.

- China removes ban on Boeing (BA) deliveries after US trade truce, via Bloomberg.

EUROPEAN TRADE

EQUITIES

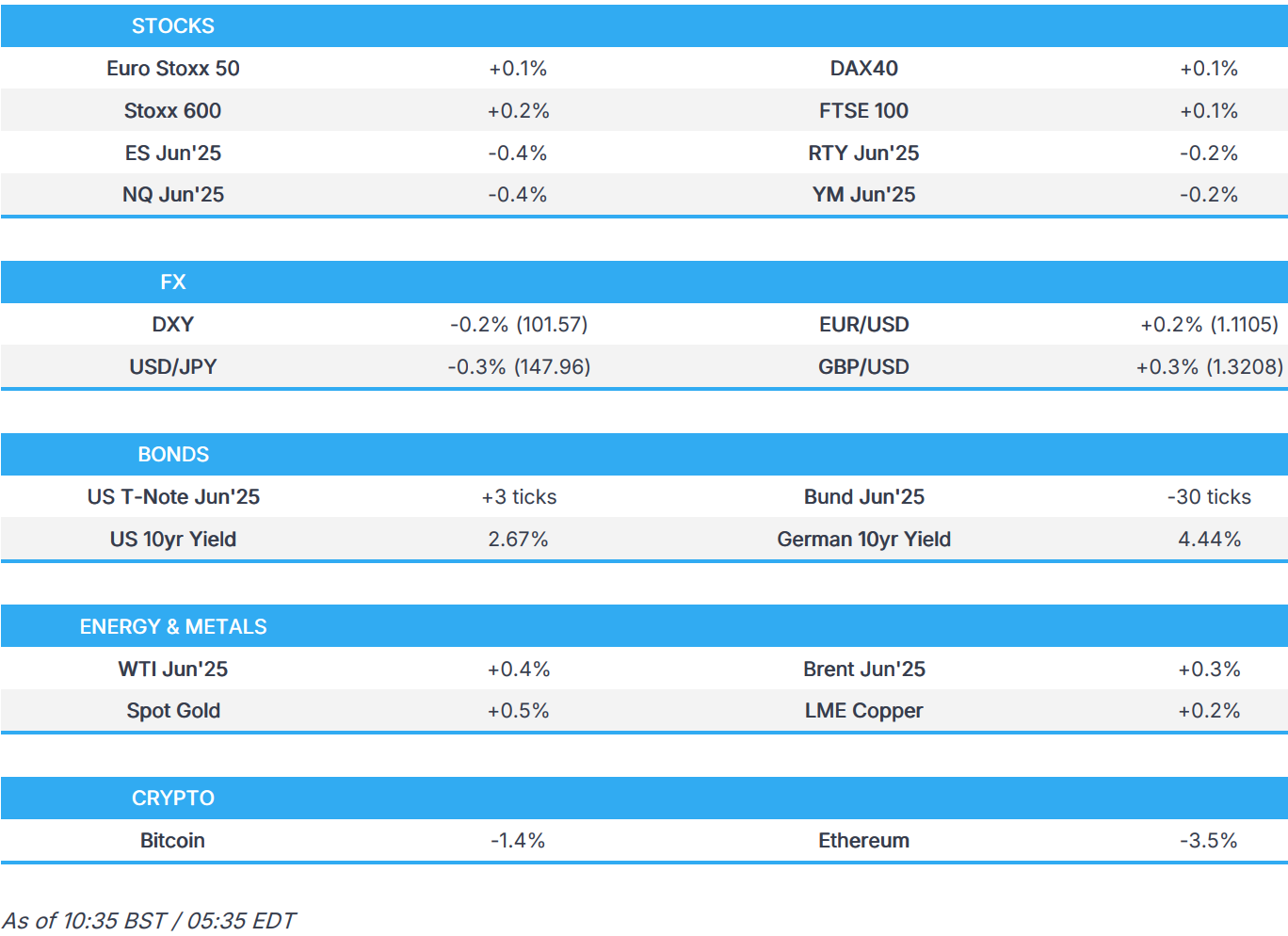

- European bourses (STOXX 600 +0.2%) are mostly, but modestly firmer as markets cool a touch from the significant upside seen in the prior session. Price action this morning has been relatively rangebound, given the lack of fresh catalysts thus far.

- European sectors hold a slight positive bias, but with the breadth of the market fairly narrow. Basic Resources leads, followed closely by Retail and Travel & Leisure to complete the top three.

- US equity futures (ES -0.4%, NQ -0.5%, RTY -0.5%) are modestly in negative territory, as the complex gives back some of the prior day’s US-China induced upside. Focus this morning has been on Bloomberg reporting which suggests China is lifting its ban on Boeing (BA) deliveries after the US-China tariff pause.

- BlackRock (BLK) CEO said it still sees global investors overweighting the US; adds that US deficits are still an issue.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY gives back some of Monday's trade-induced gains. Desks flag the uncertainty rising from the 90-day period in which both the US and China slashed their respective retaliatory tariffs by 115 bps each. Elsewhere on the docket, the highlight will be US CPI, whereby analysts expect US headline CPI to rise +0.3% M/M in April (prev. -0.1%). DXY currently resides in a narrow 101.46-101.73 range, well within yesterday's range, with the 50 DMA today at 101.86.

- EUR is relatively stable and moving in tandem with the Dollar with little action seen on ECB commentary in which ECB's Makhlouf said given effects of size, scale and more persistent nature of fragmentation-induced shocks, and their impact on prices, monetary policy responses will need careful calibration, meanwhile, ECB's Escriva said they must be humble in assessing the current situation, and ECB's Nagel said they shouldn't overreact to individual announcements. Reuters sources overnight suggested the ECB strategy review will largely endorse past policies, including QE, despite some policymakers’ criticisms, while the ECB is to keep reference to ‘forceful action’ when rates and inflation are low following the review. On the data front, May ZEW survey for Germany saw a jump in economic sentiment but an unexpected fall in current conditions - but no real follow through to the EUR.

- Haven FX are clawing back some lost ground as markets take a breather following yesterday's US-China euphoria, and following the aforementioned punchier language from Chian this morning coupled with the accompanying uncertainty provided by the 90-day de-escalation. USD/JPY resides towards the bottom of a 147.65-148.48 range, with the 50 DMA seen at 146.27 today.

- GBP is buoyed by the softer Dollar, with FX markets gaining some composure after Monday's surge in the Buck. UK jobs data this morning did little to shift the dial, with no reaction seen post-release: overall, the labour market continues to soften but at a relatively moderate rate. GBP/USD currently trades in a 1.3166-1.3216 range, well within Monday's 1.3137-1.3299 parameter.

- Antipodeans benefit from the broadly softer Dollar despite a more cautious risk tone across the markets.

- PBoC set USD/CNY mid-point at 7.1991 vs exp. 7.2188 (Prev. 7.2066).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are slightly firmer with the risk tone tepid and fixed easing from the lows seen on Monday as the dust settles following tariff announcements between the US and China. At the top-end of a 110-02 to 110-08 band. Attention for USTs is firmly on the April CPI print. A release that is perhaps slightly less pertinent given the recent US-China progress; however, it will still be scrutinised for insight into the Fed’s deliberations. After the data we have remarks from President Trump at 15:00BST in the Middle East. Reports in Axios on Monday suggested he was aiming to return with over a USD 1tln worth of deals.

- Bunds are a touch softer and, in contrast to USTs, has eked out a marginal new WTD trough at 129.43. However, despite this, the narrative is much the same as the benchmark consolidates from Monday’s marked sell off and await fresh insight on EU-US talks. On that, US Treasury Secretary Bessent was out this morning with the same type of language on the EU, describing the progress as being a little slower. On the data front, May ZEW survey for Germany saw a jump in economic sentiment but an unexpected fall in current conditions - but no real follow through to Bund price action.

- Gilts are the marginal underperformer, and in a similar fashion to Bunds the benchmark has made a new WTD low at 91.51 vs 91.63 on Monday. Gapped lower by 13 ticks at the open and then slipped a bit further to the above base. An open that followed the latest UK jobs data which, in summary, showed that the labour market continues to cool but at a gradual pace with the rate of wage growth slowing but still at a level that the MPC is unlikely to regard as being consistent with the inflation target.

- Netherlands sells EUR 1.98bln vs exp. EUR 1.0-2.0bln 2.00% 2054 DSL: average yield 3.228%.

- UK sells GBP 1bln 0.625% 2045 I/L Gilt: b/c 3.19x (prev. 3.48x) & real yield 2.23% (prev. 1.732%).

- Italy sells EUR 7.5bln vs exp. EUR 6.0-7.50bln 2.65% 2028, 3.25% 2032 & 4.45% 2043 BTP.

- Germany sells EUR 3.401bln vs exp. EUR 4.5bln 1.70% 2027 Schatz: b/c 2.2x (prev. 1.7x), average yield 1.94% (prev. 1.67%), retention 24.42% (prev. 23.72%).

- Click for a detailed summary

COMMODITIES

- Crude has traded choppily, and off the highs seen following the US-China trade deal announcement. Currently WTI & Brent are higher by around USD 0.20/bbl as traders await US CPI and updates from US President Trump who is set to give some remarks at 15:00 BST / 10:00 EDT. Brent Jul'25 sat in a busy USD 64.63-65.12/bbl range for most of the European morning, but has recently climbed out of the top-end of that range to print a peak at USD 65.35/bbl.

- Precious metals are firmer across the board, with some outperformance in spot silver as the complex benefits from the softer Dollar. Spot gold is currently higher by around USD 18/oz, and trades in a USD 3,216.06-3,265.51/oz range.

- Base metals are broadly in positive territory, benefiting from the relatively softer Dollar and mostly positive risk-tone overnight. 3M LME Copper currently trades in a USD 9,488.3-9,572.45/t range.

- China crude oil supply to China set to hold steady at around 47.5mln barrels in June, via Reuters citing sources.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK ILO Unemployment Rate (Mar) 4.5% vs. Exp. 4.5% (Prev. 4.4%); Employment Change (Mar) 112k vs. Exp. 120k (Prev. 206k)

- UK Claimant Count Unem Chng (Apr) 5.2k (Prev. 18.7k, Rev. -16.9k); UK HMRC Payrolls Change (Apr) -33k (Prev. -78k, Rev. -47k)

- UK Avg Wk Earnings 3M YY (Mar) 5.5% vs. Exp. 5.2% (Prev. 5.6%, Rev. 5.7%); Ex-Bonus (Mar) 5.6% vs. Exp. 5.7% (Prev. 5.9%)

- UK BRC Retail Sales YY (Apr) 6.8% (Prev. 0.9%); Total Retail Sales 7.0% (Prev. 1.1%)

- EU ZEW Survey Expectations (May) 11.6 (Prev. -18.5)

- German ZEW Economic Sentiment (May) 25.2 vs. Exp. 11.9 (Prev. -14.0); ZEW Current Conditions (May) -82.0 vs. Exp. -77.0 (Prev. -81.2)

NOTABLE EUROPEAN HEADLINES

- Barclaycard UK April Consumer Spending rose 4.5% Y/Y, which was the biggest increase since June 2023.

- ECB strategy review will largely endorse past policies, including QE, despite some policymakers’ criticisms, while the ECB is to keep reference to ‘forceful action’ when rates and inflation are low following the review, according to sources cited by Reuters.

- ECB's Makhlouf says given effects of size, scale and more persistent nature of fragmentation-induced shocks, and their impact on prices, monetary policy responses will need careful calibration.

- BoE's Chief Economist Pill says should not assume that latest MPR forecasts is a direct endorsement of market interest rate curve; worried about potential risks to inflation He does see risk of second round effects. Remain concerned that they've seen a structural change in price and wage setting within the UK. The response of monetary policy to ensure they get inflation back to target may need to be more persistent.

NOTABLE US HEADLINES

- WSJ's Timiraos posted that Goldman Sachs shifted the timing of its next expected Fed cut to December from July, while it stated "In light of these developments and the meaningful easing in financial conditions over the last month, we are raising our 2025 growth forecast by 0.5pp to 1% Q4/Q4 and reducing our 12-month recession odds to 35%" and "lowered our core PCE inflation path to peak at 3.6% (vs. 3.8% previously)".

- US President Trump posted "We are going to slash the cost of prescription drugs, and we will bring fairness to America. Drug prices will come down—We're gonna cut out the middlemen and facilitate the direct sale of drugs at the most favored nation price directly to the American citizen!"

- BofA Fund Manager Survey (pre-US/China trade update): Global fund managers most underweight US dollars in May since 2006 61% of fund managers see soft landing for the economy versus 37% in April; 26% see hard landing, down from 49% in April. Prior to US/China Geneva talks, fund managers saw US tariffs on China goods at 37%. "Positive US-China trade war ceasefire prevents recession/credit event".

GEOPOLITICS

MIDDLE EAST

- US Secretary of State Rubio said the State Department is sanctioning three Iranian nationals and one Iranian entity with ties to Iran's organisation of defensive innovation and research.

RUSSIA-UKRAINE

- Russian Foreign Minister Lavrov discussed with his Turkish counterpart issues related to May 15th direct talks with Ukraine.

- US State Department said Secretary of State Rubio discussed a path to peace and a ceasefire in Ukraine with French, German, Polish and Ukrainian foreign ministers as well as the EU High Representative.

- Senior Kyiv Official says Ukrainian President Zelensky will meet Russian President Putin, and not other members of the Russian delegation on Thursday in Turkey.

CRYPTO

- Bitcoin is a little lower and trades just beneath USD 103k; Ethereum extends losses and sits just shy of USD 2.5k.

APAC TRADE

- APAC stocks traded mostly higher following the rally on Wall St owing to the US-China trade war de-escalation after both sides agreed to cut tariffs by 115ppts for an initial period of 90 days, although some of the gains were capped as the euphoria began to moderate.

- ASX 200 edged higher amid outperformance in tech and energy but with further advances contained by weakness in defensives and gold miners.

- Nikkei 225 rallied to above the 38,000 level following the cooling in US-China trade tensions but with the index off intraday highs amid some profit-taking and a slight pullback in USD/JPY, while BoJ rhetoric continued to signal future hikes if prices and the economy improved.

- Hang Seng and Shanghai Comp lagged despite the de-escalation in the US-China trade war which the Hong Kong benchmark already had its opportunity to react to yesterday, while questions lingered on what will happen during the 90-day reprieve as the trade deficit remains and the current 30% tariff on Chinese goods still a relatively high level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Summary of Opinions from the April 30th-May 1st meeting stated that one member said the central bank is likely to continue raising interest rates in line with improvements in the economy and prices, while a member said the BoJ must make policy decisions without preconception as uncertainty over the outlook is very high. There was also the opinion of no change to the BoJ's rate-hike stance as real interest rates are deeply negative, but risks must be scrutinised and the BoJ has little choice but to take a wait-and-see stance until developments surrounding US trade policy stabilise to some extent. Furthermore, a member said that uncertainty surrounding economy and price outlook is high and the likelihood of achieving price goal is not as high as in the past, while it was stated that the BoJ will enter a temporary pause in rate hikes but shouldn't slide into excessive pessimism and must guide policy nimbly and flexibly.

- Nissan (7201 JT) 2024/2025 (JPY): operating profit 69.8bln (-87.7%), net -670.90bln (prev. 426.65bln), Revenue 12.63tln (prev. 12.69tln); withholds FY guidance due to tariffs, will consolidate production plants to 10 from 17. Nissan impact on Renault (RNO FP) Q1 net estimated at EUR 2.2bln loss.

- JD.com (JD/9618 HK) Q1 (USD): EPS 1.16 (exp. 1.05), Revenue 41.5bln (exp. 40.2bln); Co. notes of improving consumer sentiment.

DATA RECAP

- Australian Westpac Consumer Sentiment (May) 92.1 (Prev. 90.1)

- Australian NAB Business Confidence (Apr) -1.0 (Prev. -3.0)

- Australian NAB Business Conditions (Apr) 2.0 (Prev. 4.0)

Loading...