Season-End Summary of Challenges under Rule 14a-8

The SEC has just completed its oversight role for the 2024/2025 season over challenges brought by companies to exclude proposals submitted by their shareholders per Rule 14a-8. What follows is a summary of the results for this season with comparisons to prior seasons.

Under Rule 14a-8, companies generally must include shareholder proposals in their proxy statements to be considered at the annual meeting. The rule, however, provides several bases for exclusion, including 13 substantive requirements that proposals must comply with to avoid exclusion – Rule 14a-8(i)(1) to (i)(13) – as well as procedural requirements for when and how they must be submitted to the companies by shareholders. The rule has a process for how companies can seek to exclude these proposals by submitting a challenge to the SEC to obtain a favorable ‘no-action letter.’

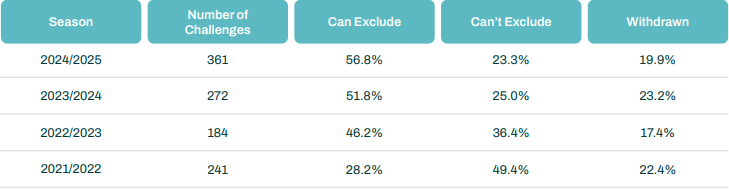

Challenges were up 33 percent from last season, and 96 percent from the season before

SEC’s SLB 14M rescinds SEC’s SLB 14L

SLB 14L (2021): The SEC adopted Staff Legal Bulletin 14L in November 2021, which rescinded staff legal bulletins 14I, 14J and 14K, and made it more difficult to invoke the 14a-8(i)(7) ‘ordinary business’ exception with proposals that raise issues of broad social or ethical concern related to the firm’s business. In the first season after its adoption, we saw a marked increase in the number of such proposals and a drop in the number which were challenged, particularly those related to environmental and social issues. SLB 14M (2025): In a reversal of policy the SEC adopted Staff Legal Bulletin 14M in February 2025 which rescinded SLB 14L and thereby turned back the clock on its 14a-8 practices to where things stood before the SEC issued SLB 14L in 2021. SLB 14M has had a significant effect on no-action challenge requests, particularly for those that invoke the (i)(7) “ordinary business” exclusion and the (i)(5) “economic relevance” exclusion, as discussed below.

Season over Season Observations

1. Challenges have increased 96% since the 2022/2023 season, especially for those that invoke the (i)(7) ‘ordinary business’ exception which went from 30 in the 2022/2023 season to 58 in the 2023/2024 season, and to 85 in the 2024/2025 season.

2. Over the past four seasons, proponents’ ‘success rate’ of “Can’t exclude” has steadily declined season-over-season: 49.4%, 36.4%, 25.0%, 23.3%.

3. Over the past four seasons, the number of successful challenges under the (i)(7) ‘ordinary business’ exception has increased in number season-over-season: 20, 30, 58, and 85.

4. We attribute the recent increase to 85 to the SEC’s adoption of SLB 14M.

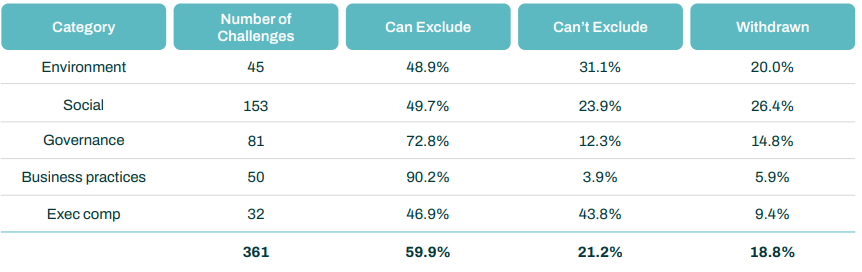

By Category

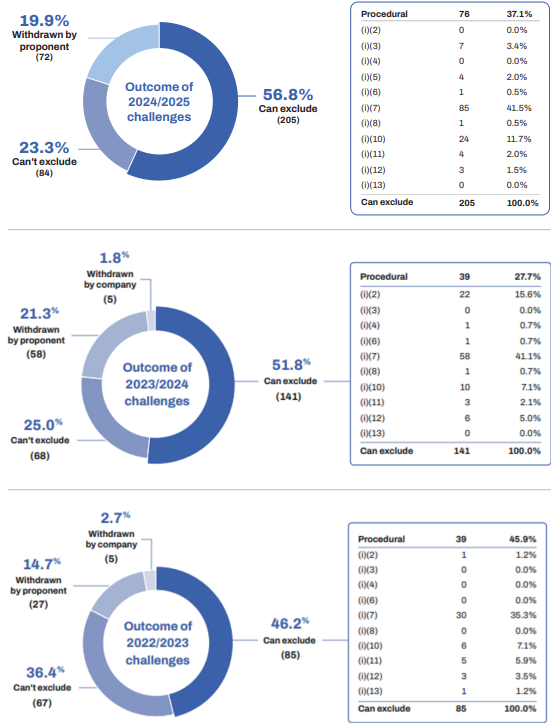

Since we initiated our coverage of 14a-8 matters, we’ve used five categories to segment 14a-8 proposals: Environment, Social, Governance, Business Practices and Exec Comp. There’s a high correlation between Business Practices and challenges brought under the (i)(7) ‘ordinary business’ exception. Here’s the breakdown for 2024/2025 season.

Spotlight on (i)(7)/(i)(5) Challenges post-SLB 14M

In response to the SEC’s issuance of SLB 14M, the number of (i)(7)/(i)(5) challenges nearly doubled. But the relative success rate went down from 69.8% to 58.3%.

• We attribute this to many Challenges being brought after SLB 14M was issued that wouldn’t have been brought during the 2024 season.

• In our databases we label Challenges by proposal type. E.g. “DEI efforts.” SEC rulings varied for a given proposal type.

• E.g., All “collective bargaining rights” and “Bitcoin investment” proposals were excludable.

• E.g., Out of 26 “lobbying” proposals only two were required to be included.

• E.g. Out of 21 emission-related proposals, eight were excludable and two were withdrawn

Notes

• We define the ‘14a-8 season’ based on annual meeting dates scheduled between July 1 and June 30 of the following calendar year.

• Procedural grounds for exclusion are set forth in Rule 14a-8(b)-(f) and include failure to submit the proposal by the required date and failure to adequately prove ownership of shares that are beneficially held in ‘street name’.

Rule 14a-8

DragonGC has been tracking 14a-8 developments with two databases and frequent reports on the trends that we see. One database tracks proposals that have been included in annual proxy statements and the voting results thereon. For this season, we’ll continue this coverage for annual meetings through June 2025, with a season-end summary in July 2025. The other database, which we used to prepare this report, tracks challenges to inclusion brought by companies per Rule 14a-8.

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release