Tariffs, Targets and Transparency

ACCOUNTING FOR UNKNOWNS is always the most challenging aspect of executive compensation design—and that exercise is shaping up to be particularly tricky this year. In addition to ongoing external forces like geopolitical tension and inflationary pressure, boards now also face uncertainty around tariffs as they address goal-setting and incentive pay practices.

“How tariff actions will actually unfold and what impact those actions will have on businesses and industries are still unknown,” says Alexa Kierzkowski, a managing director at FW Cook. “And the challenge of ensuring that payouts align with actual performance is that much more difficult when boards are dealing with the prospect of an exogenous item that is out of everyone’s control.”

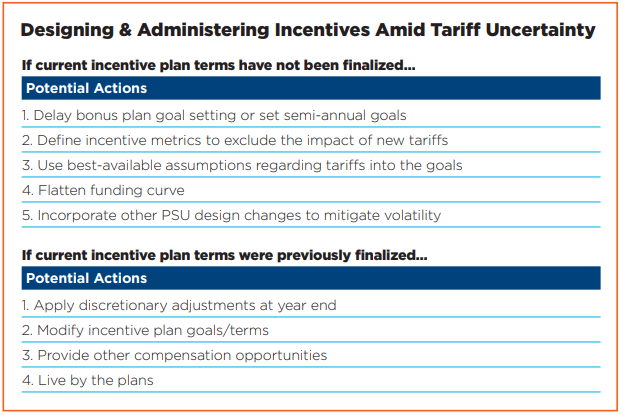

Timing will also factor heavily in how compensation committees anticipating an impact on operational performance can approach addressing tariff uncertainty in their compensation plan design. Companies grappling with the challenge fall into two camps—those that have yet to finalize their plan terms for the year and those that have already established goals and incentive pay terms, which includes most companies with a December 31 fiscal year end.

PRE-PLAN DESIGN OPTIONS

Some companies still in the design phase of annual incentive pay planning when tariff actions were initially announced opted to postpone goal-setting. “In some cases, companies set first-half goals and delayed goal-setting for the second half of the bonus plan due to the uncertainty related to tariffs,” says Kierzkowski, who adds that as hope of the picture clarifying dwindles, compensation committees seeking to proactively account for external disruptions in their incentive pay programs can consider four approaches:

Incorporating best available assumptions into goal-setting. One approach is to move forward with setting goals, factoring in the estimated impact of tariffs. “The challenge there is that there’s a ton of ambiguity about that impact,” says Metin Aksoy, a managing director at FW Cook. “Tariffs are not a one-time external item that is easily quantifiable. There are primary, secondary and tertiary impacts, so in trying to define exactly how they will affect your operating goals you could be totally wrong.”

For example, a manufacturer that imports parts may be able to calculate the impact of a 20 percent tariff on its costs of goods sold. But secondary impacts, such as a reduction in demand due to counter-tariffs on products it exports or the possibility that a price increase can offset the hit to its profit margin, are less easily predictable. “What if you set goals assuming that the entire 20 percent would directly impact profits, but it turns out you’re able to pass 15 percent of that on to your customers?” asks Aksoy. “That would become an unanticipated windfall. So the idea of incorporating the impact of tariffs into goals sounds pretty clean, but it’s not an easy mathematical adjustment.”

Excluding the impact of tariffs. Another approach is to set goals and adopt a framework of adjustment parameters that a company can track against on a quarterly basis. This allows room for discretion if trade policy decisions are found to materially dampen—or boost—incentive payouts based on meeting performance goals. “That way you’re building a framework around quantifying the impact and updating it as you go along, as opposed to a simple discretionary, ‘We’re going to add 20 percent to the bottom line,’” explains Kierzkowski.

When including the impact of tariffs in a list of potential adjustments in calculating operating results, companies will need to define the measure that will be used for the adjustment. “It’s important to note that while an exclusion can be discretionary for cash-based bonus pay—‘may adjust’—it needs to be mandatory—‘shall adjust’—for equity incentives,” Kierzkowski notes. “Otherwise it will generally be considered an accounting modification that will likely trigger an increased award expense and disclosure requirements.”

Flattening the funding curve. Widening the range of performance outcomes that allow for a performance payout is another way to mitigate the risk that external shocks outside of management’s control will distort financial outcomes. “This is something you want to do on both the upside and the downside,” cautions Kierzkowski. “Instead of just providing downside protection, you should moderate payouts on both sides of the range.”

Performance share unit design changes. Shifting from absolute performance metrics to relative metrics measured against a peer group can help ensure management is rewarded for outperformance amid macroeconomic factors affecting an entire industry. However, identifying an appropriate peer group and ensuring an apples-to-apples comparison with and among the peers can be challenging.

Breaking long-term PSU incentive programs into annual grants with distinct goals is another way to reduce the risk that goals set at the start of a three-year cycle become unattainable due to unforeseeable disruptions. “But going that route means making three grants that will show up on three proxy tables, which is likely to garner criticism for not having truly long-term goals,” warns Kierzkowski, who advises setting goals for one-year periods upfront instead. “For example, you can have each year be a percentage growth off of the previous year so that you’re establishing long-term goals but mitigating volatility by giving each one a different starting place.”

POST-DESIGN POSSIBILITIES

Companies that finalized their pay programs before tariff developments can also weigh actions to aim to align bonus payouts with actual performance without undermining the integrity of the plan:

Applying discretion. One option is to retain flexibility by waiting for the impact of tariffs to play out and, if warranted, make a discretionary adjustment to bonus plan funding at yearend. “While investors and proxy advisors dislike discretion, undeniably strong performance can help offset concerns,” says Kierzkowski. “But if the company applying discretion is at a medium or high level of concern on ISS’s quantitative pay-for-performance test or ends up funding an above-target award, that could be a tough pill for a lot of shareholders and proxy advisors to swallow.”

Modifying bonus plan terms. Amending bonus plans to exclude the impact of tariffs may have better optics than making discretionary changes at the end of the performance period.

Resetting performance goals midyear. While modifying current year goals midstream is also an option, most companies lack sufficient visibility to reset goals with confidence, and the action is likely to be viewed as “moving the goalpost” and invite stakeholder scrutiny

STAYING THE COURSE

Even among companies likely to be impacted by tariff actions, some will opt out of addressing the potential impact of tariff actions in their incentive pay programs, notes Aksoy. “Some companies will follow the ‘do nothing’ philosophy that they need to ride and die with the shareholders on this.”

A “do nothing” approach signals a commitment to accountability, avoids any perception of insulating management from outcomes affecting shareholders and sidesteps the governance and communication complexities that come with making potentially problematic changes. However, it also poses risks and can undermine the overarching intent of incentive programs.

“You shouldn’t lose sight of what the incentive plan is for, which is to motivate behaviors and isolate for management effectiveness,” says Aksoy. “If you take the position that the company won’t consider changes, people may feel they’re out of the game due to an exogenous event over which they have no control. And that’s not going to drive the behaviors it’s intended to drive.”

Companies concerned about talent retention due to underwater PSUs can incorporate other PSU design changes to help mitigate volatility, notes Kierzkowski. “Rather than risking governance backlash by applying discretion or taking a special action, you could look toward making your go-forward program more attractive,” she explains. “Keeping the equity grants you already gave the same but offering a more enticing go-forward program may avoid entering a heightened category of scrutiny related to special grants and adjustments to existing plans.”

Ultimately, however, no approach other than doing nothing is guaranteed to pass muster with shareholders and proxy advisors. “There is disclosure and say-on-pay risk associated with anything that you do,” says Aksoy. “It’s a judgment call where individual circumstances such as how tariffs will impact your industry and the retention value your business has will determine what is best. So make sure that you’re comfortable with your rationale for whatever action you decide to take and can explain it. Because at the end of the day, it will come down to how big the impact is and how fair and balanced it seems to stakeholders.”

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release