The effects of the Emissions Trading System on European investment in the short run

Prepared by Pablo Anaya Longaric, Virginia Di Nino and Vasileios Kostakis

Published as part of the ECB Economic Bulletin, Issue 8/2024.

This box takes stock of the impact of the EU Emissions Trading System (EU ETS) on European investment, while testing empirically the effect of carbon pricing on international and domestic investment flows. The EU ETS has reduced greenhouse gas emissions, bringing long-term benefits for the environment, the European economy and Europe’s energy independence. Empirical evidence on the long-term benefits indicates that the ETS also triggers green investment to reduce the carbon intensity of firms’ production processes.[1] When compared with alternative policy instruments, carbon pricing is shown to be an efficient mechanism for providing incentives for the adoption of low-carbon technologies.[2] As a result, the ETS is instrumental in enhancing European energy independence from fossil fuels.

However, it is not immediately clear how investment has been affected in the short term. The environmental benefits might come at the cost of reduced investment since carbon pricing works as an energy tax levied on companies.[3] It might also divert investment towards countries that have not put in place comparable legislation to limit carbon emissions through pricing or taxation – so-called “carbon leakage”. At the same time, it could provide incentives for firms to invest in green technologies, while ETS revenues, through EU programmes such as the Innovation Fund, Modernisation Fund and the REPowerEU component of the Recovery and Resilience facility, are deployed to stimulate green investment. As there is not yet a clear consensus on the effect on investment, an investigation into which of these forces have so far prevailed would help to fine-tune environmental policies so as to limit the risk of carbon leakage and mitigate possible economic costs.

The analysis below examines the impact of changes in the carbon price on international and European investment flows. It estimates the effects of carbon price shocks on greenfield foreign direct investment (FDI) and on gross fixed capital formation over time at both the country level and the sectoral level. To identify carbon price shocks, changes in the prices of futures contracts for emissions allowances that occur around the time of changes in the ETS regulations are included as an instrument in a vector autoregressive model.[4] Importantly, the analysis focuses on the near-term costs associated with carbon pricing, whereas the long-term benefits of cleaner energy and reduced dependence on fossil fuels are beyond the scope of the box.[5] The sample spans 2003-19, incorporating the period from the announcement of the implementation of the ETS until the end of the third phase of implementation. It excludes the pandemic period, when other types of major shock took place that could contaminate the analysis, but includes carbon price shocks associated with announcements in 2019 about future changes in the ETS regulations.

Empirical analysis suggests that flows of greenfield FDI in Europe are dampened temporarily when the carbon price rises. Following a carbon price shock normalised to result in a 1% increase in the energy component of the producer price index (PPI) – which corresponds to raising carbon futures prices by 25% on impact – flows of European greenfield FDI into non-European countries rise significantly (Chart A, panel a).[6] Moreover, FDI between non-European countries increases after a year. Similarly, there is a decline in European inward greenfield FDI flows, both from outside and from within Europe, with the latter continuing to contract over the medium term (Chart A, panel b). Overall, these reactions suggest that there might be a temporary diversion of funds away from Europe when carbon prices increase.[7]

Chart A

The impact of a carbon price shock on global greenfield FDI

a) Impact of a carbon price shock on FDI in the rest of the world |

b) Impact of a carbon price shock on FDI in Europe |

|---|---|

(y-axis: percentage changes; x-axis: years after impact) |

(y-axis: percentage changes; x-axis years after impact) |

|

|

Sources: Eurostat, FT fDi Intelligence and ECB staff calculations.

Notes: “ROW” stands for “rest of the world”. The chart shows the estimated effects on announced projects for greenfield FDI stemming from a carbon price shock that leads to a 1% increase in PPI energy on impact. The sample spans 2003-19. As the ETS became operational in 2005, the extended time series does not substantially influence the results. The specification follows , where is the outcome variable of interest at horizon h between countries i and j, and includes a set of macroeconomic controls, including the lagged dependent variable. The solid lines show the estimated impulse responses, while the shaded areas represent 90% confidence intervals based on Driscoll-Kraay standard errors robust to serial correlation and cross-section dependence.

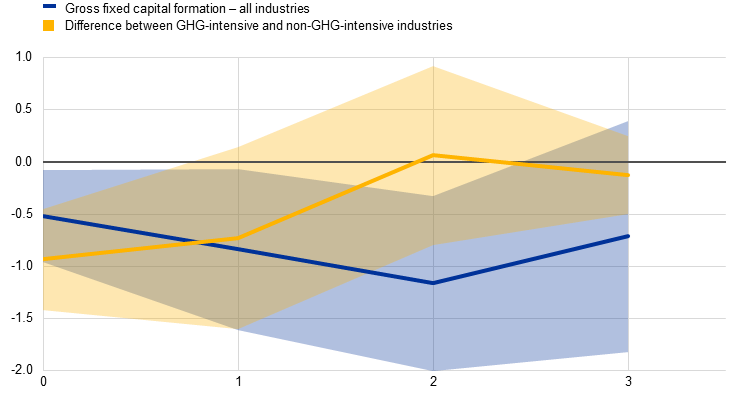

There also seems to be an adverse effect on domestic investment in Europe. In response to a carbon price shock that increases PPI energy by 1%, EU gross fixed capital formation falls by 0.5% in the first year, and the cumulative decrease amounts to more than 1% after two years (Chart B). It should be noted, however, that the level of uncertainty surrounding the estimates is high. This decline occurs because higher carbon prices act as a tax on firms’ production and reduce overall economic activity, outweighing increased investment to rebalance firms’ production processes towards green energy sources.

Chart B

The impact of a carbon price shock on gross fixed capital formation in the EU

(y-axis: percentage changes; x-axis: years after impact)

Sources: Eurostat and ECB calculations.

Notes: “GHG” stands for “greenhouse gas”. The chart shows the estimated effect of a carbon price shock that leads to a 1% increase in PPI energy on impact. The specification is the same as the specification described in the notes to Chart A. Greenhouse gas-intensive sectors are those that have emissions (in proportion to their value added) greater than the median.

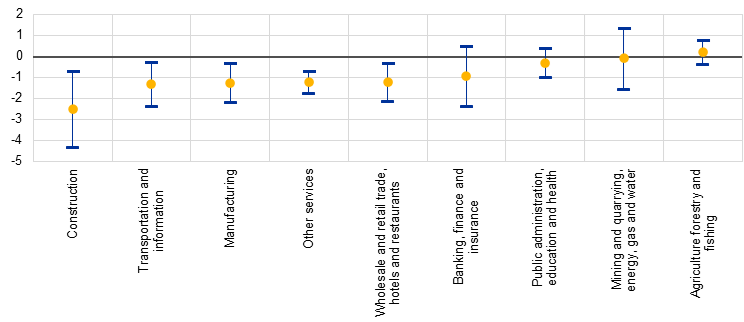

High-carbon sectors are the main industries affected by the carbon price shock.[8] The decrease in aggregate investment is driven mostly by the construction, transportation and manufacturing sectors (Chart C). Moreover, mining and quarrying, despite being very carbon-intensive activities, have not been significantly affected by carbon price shocks. This is most likely due to the rollout of free allowances in this sector.[9]

These findings should be seen in the context of other studies which show that the ETS has neither reduced economic activity nor led to significant carbon leakage.[10] In fact, the reduction in carbon emissions achieved through the ETS is largely attributed to genuine decreases in emissions rather than shifts in production to regions with laxer environmental regulations. In addition, European examples show that when carbon pricing is complemented with ambitious government support for advanced technology, they can be mutually reinforcing and make the business case for investing in decarbonisation.[11]

Chart C

The impact of a carbon price shock on gross fixed capital formation in the EU, by sector

(percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The whiskers show the impact on each sector. The groupings follow the methodology of Känzig, op. cit., as also employed in Matzner and Steiniger, op. cit. The regression specification is the same as described in the notes to Chart A.

The analysis suggests that higher carbon prices may temporarily dampen domestic investment and shift global FDI away from Europe, but the longer-term benefits can largely outweigh these short-term effects.[12] A more comprehensive analysis that also looks at the long-term benefits related to achieving independence from fossil fuels and enhancing European energy independence is warranted. In parallel with tighter regulations in terms of coverage of sectors and emission entitlement rights, the European Commission has introduced a carbon border adjustment mechanism (CBAM). This contributes to shielding European businesses from possible unfair foreign competition and to restoring level playing fields by charging EU importers a price proportional to the emissions entailed in foreign production processes.[13] Together with complementary policies that are currently under discussion, this will sustain Europe’s future production capacity and its external competitiveness.[14]

Distribution channels: Banking, Finance & Investment Industry

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release